Аннотация к книге "Variance Estimation for Bayesian Dynamic Linear Models. Inference for Multivariate State Space Models"

Time series modelling and in particular multivariate time series have received considerable attention in the literature over the past 20 years. Time series data are met in almost all subject areas, such as in economics, engineering, medicine and genetics, to name but a few. One of the key problems of multivariate time series analysis is the estimation of the covariance matrix of the data, as this holds important information of the co-evolution and correlation of the component time series data...

Time series modelling and in particular multivariate time series have received considerable attention in the literature over the past 20 years. Time series data are met in almost all subject areas, such as in economics, engineering, medicine and genetics, to name but a few. One of the key problems of multivariate time series analysis is the estimation of the covariance matrix of the data, as this holds important information of the co-evolution and correlation of the component time series data of interest. The aim of this book is to provide an account of the recent developments on this subject area and subsequently to develop methodology for tackling the problem of variance estimation in time series. The book introduces the basic modelling framework for state space time series models and then it provides estimation algorithms, within the Bayesian paradigm, for several classes of models. The book is aimed at both masters/Ph.D. students in a numerate discipline (such as statistics, mathematics, economics, engineering, computer science, and physics) and postdoctoral researchers interested in time series methods.

Данное издание не является оригинальным. Книга печатается по технологии принт-он-деманд после получения заказа.

Шесть кроликов гуляли по краешку земли, огромную морковку шесть кроликов нашли. Может быть, сделать из нее дом? Или корабль? А что если это морковка-самолет? Что кролики сделали с этим невиданным чудом - узнаем, прочитав книжку. Эту веселую историю придумала художница Сатое Тоне. Она родилась в Японии, в последние годы живет и работает в Италии. В 2013 году художница стала лауреатом Международной...

Это свет, который таится во всех чудесах и прелестях мира… Включая тебя! На обложке удивительной книги Аарона Бекера — солнце в окружении разноцветных окошек. Поднеси её к свету, и ты увидишь, как от страницы к странице меняются цвета, добавляя к палитре светящихся красок всё новые оттенки. Эта книга — изящная ода солнечному свету, который согревает землю, дарит жизнь и рождает чудеса мира, одно из...

Омерзительное искусство — это новый взгляд на классическое мировое искусство, покорившее весь мир. Софья Багдасарова — нетривиальный персонаж в мире искусства, а также обладатель премии "Лучший ЖЖ блог" 2017 года. Знаменитые сюжеты мифологии, рассказанные с такими подробностями, что поневоле все время хватаешься за сердце и Уголовный кодекс! Да, в детстве мы такого про героев и богов точно не читали…...

Издательство:

Эксмо-Пресс

Дата выхода: декабрь 2018

На свете есть поросята, ежата, совята, лягушата, утята, гусята… …а как же называли Киппера, когда он был маленьким? Для детей дошкольного возраста. Художник: Мик Инкпен. Переводчик: Артем Андреев.

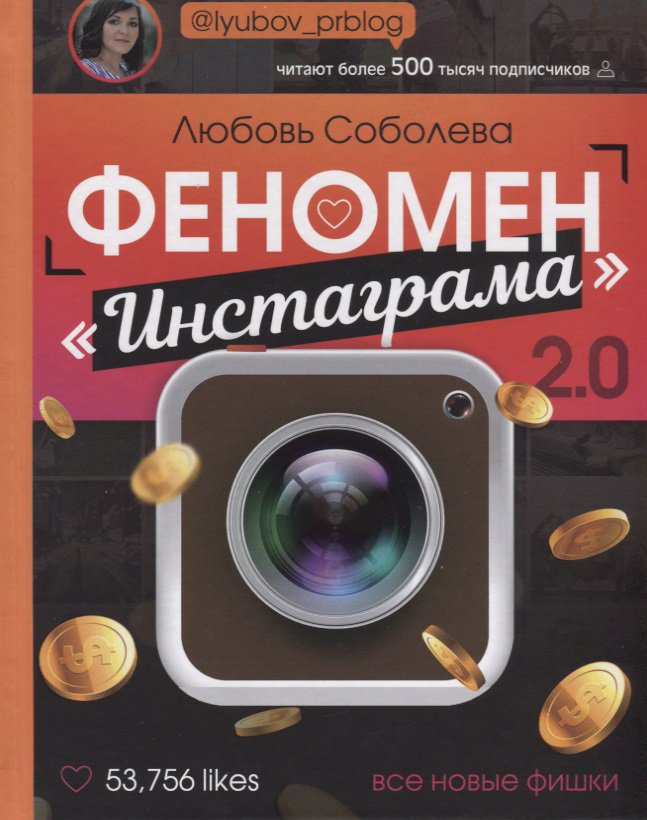

Для чего вы заходите в «Инстаграм»? Посмотреть, как дела у знакомых? Выложить фотографии со вчерашней вечеринки? Развеяться и отдохнуть? Лично я вот уже два года захожу в «Инстаграм», чтобы заработать. Немного цифр, которые лучше любых слов объяснят вам, чем может быть полезен «Инстаграм»: -17 000 000 чистой прибыли у медицинской клиники в месяц (полтора года назад ее не существовало вообще); -60 000 000...

Оставить комментарий